Table of Contents

- Preamble

- Why should you invest?

- What can you invest in?

- Intermission

- Funds

- Special Cases and Considerations

First thing's first

- I am not providing personal investment advice, and I am not a licensed investment advisor.

- Any investments you make are done at your own risk. I am not liable for any actions or inactions you take.

- All information I am presenting is for informational purposes only, and should not be considered financial advice.

- tl;dr: Please don’t sue me.

Investing may not be for you if…

You have high interest rate debts:

- student loans, credit cards, gambling, …

- Do you think that the investment will give you more money than the debt is costing?

- With any debts, consider the cost-benefits of investing -vs- paying it off

You don’t have an emergency fund:

- 3-6 months of living expenses set aside

- Don’t put this in anything more than savings account or money market*

- If things get rough for whatever reason, you’ll want this to be liquid

Why should you invest?

Inflation

Inflation is...

- Every day, a dollar is worth a little bit less than it was the day before

- Recently, we’ve been at around 2% per year

- If you could buy a pack of gummy bears last year for $1, they’ll now cost about $1.02

- After 5 years, $1.10

- After 10, $1.22

- Pretty soon, gummy bears are a .01%-er luxury good (Damn you, Bill Gates and your delicious gummies!)

- Or maybe they’ll do something sneaky like put fewer in a pack… **cough cough ice cream cough**

Let's take a look at some graphs of inflation over time.

First we have a long range chart, 1958 - 2017:

There's a lot of crazy stuff happening up through the 80s, but more recently it's calmed down immensely.

There's a lot of crazy stuff happening up through the 80s, but more recently it's calmed down immensely.

Next, let's look at a more recent view, 2000 - 2017:

The Fed has made it a goal to keep inflation around 2%*, and we can see that we're right about there on any given year.

If your investment returns are greater then that, then your money is growing in value. If it's less, then you're losing value.

The Fed has made it a goal to keep inflation around 2%*, and we can see that we're right about there on any given year.

If your investment returns are greater then that, then your money is growing in value. If it's less, then you're losing value.

Your money can "work" for you

- “Investing” can help combat the corrosive effects of inflation*

* It can also help increase your wealth

- The general idea is to let other people or businesses use your money now on the promise (or hope) of getting more in the future

What can you invest in?

- Real Estate

- Commodities (oranges, gold, bitcoin)

- Currency (forex)

- P2P Lending

- And many more!

Savings Accounts

- A bank account that earns interest

- FDIC insured up to $250,000

- Low volatility (how much the rate of return will change over time)

- Good for short term savings

- ~0.01%-2% return*

* rates probably out of date

- 1.65% Synchrony

- 1.60% Ally

- 1.55% CIT Bank

- 1.55% Discover

- ----------------

- 0.05-0.15% USAA

- 0.01% Chase, Wells Fargo, Bank of America

Money Market

- Short term loans to companies or banks

- Usually 1 year or less

- Can directly invest, or go through a bank account

- Low volatility

- Good for short term savings

- ~0.1-2.0% return

- May want to skip these right now while their return is lower than a good savings accounts

Bonds

- Buying and selling loans

- Corporate

- Government T-Notes (US)

- Moderate Volatility with higher grades

- Different “grades” for estimating risk/reward

- Investment (lower return, lower risk)

- Junk/High yield (higher return, higher risk)

Stocks

- Represents a stake in some corporation

- You may vote in shareholder meetings

- You may receive a portion of the company’s profits

- Can sell your share to someone else

- Profits

- You either receive regular dividend payments

- Or that money is reinvested in the company

- Price of a stock is (loosely) tied to the profitability of the company

- Higher volatility

And now a brief intermission...

Feel free to take a bathroom break, make some coffee, walk the dog, or make a large purchase on a perfectly legitimate website .

Choosing is hard

You may be thinking to yourself,- ~80% of managers don’t beat the S&P indices over a 1 year period

- 85-91% of managers don’t beat the S&P indices over a 10 year period

The Market

When people talk about "The Market" doing [well|poorly], they're generally talking about the S&P 500 or some other similar index of companies. In the example of the S&P 500, it "tracks" 500 large companies like Google, AT&T, and 3M. You can find the full listing here. With any index, the value of each component company is weighted and combined, giving a value for that index, in this case, listed as SPX.

So, if someone says that the Economy is doing poorly today as evidenced by the S&P 500 being down, say 5 percent, that means that of the companies that make up the S&P 500, more of them are doing worse than good - enough so to move the value of all of them down. Any given index being "down" or "up" doesn't reflect what the entire economy is doing, just the general movement of those companies involved. The actual formulation that describes how each company contributes to the movements of a given index is beyond the scope of this course, but if you're interested in that, the info is publicly available.

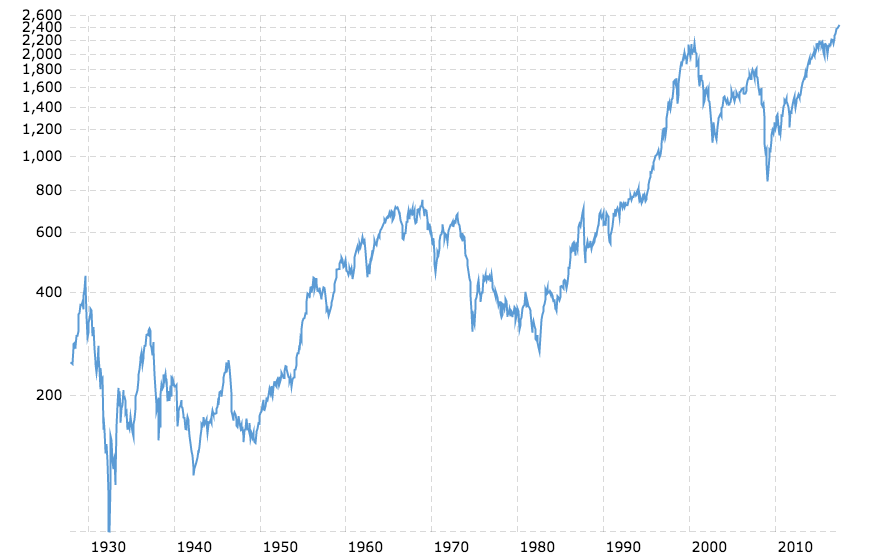

So, let's take a look at historical returns of the S&P 500

Log Scale

Something you don't usually see when looking at stock charts is the logarithmic scaled chart. An advantage this gives you is that you are able to see percentage increases linearly (i.e. a 6% increase from 100 looks the same as a 6% increase from 100000).

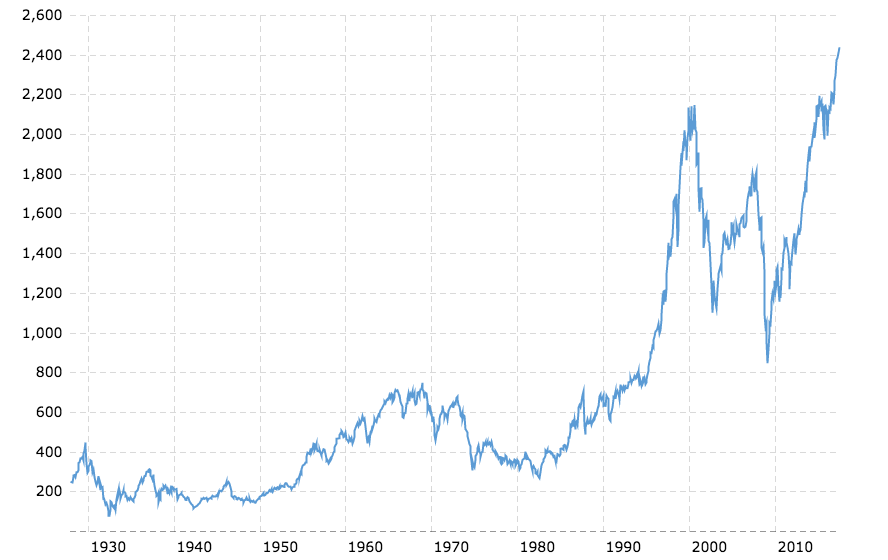

Linear Scale

Much harder to interpret.

Next, let's look at how things turn out over time.

Best and Worst N-year periods of the S&P 500, annualized return

| 1 | 5 | 10 | 15 | 20 | 25 | |

|---|---|---|---|---|---|---|

| Best | 52.56% | 28.44% | 21.56% | 19.45% | 18.38% | 17.86% |

| Worst | -43.84% | -8.42% | 0.65% | 3.68% | 5.63% | 8.09% |

The above table shows the best and worst 1, 5, 10, 15, 20, and 25 year periods of the S&P 500, going all the way back to 1929. To create these numbers, I used data from http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html and the magic of spreadsheets to generate these geometric averages.

In any given year, an index like this can have massive swings. However, if you're able to ride out the storm, investing in an index like this has historically been pretty good, yielding an 8% annual return over the worst 25-year period.

Other fun S&P 500 things:

- Average S&P 500 return/year:

- 1928-2016: 11.42%

- 2007-2016: 8.64%

- Fun fact: if you invested $100 in 1928 in the S&P 500, you’d have a cool $328,584.46 now

You'd also be dead.

Let's reiterate:

- ~80% of managers don’t beat the S&P indices over a 1 year period

- 85-91% of managers don’t beat the S&P indices over a 10 year period

Funds

Funds take some subset of investments (US Large Capital Stocks, European Junk Bonds, etc) and bundle them in a way that's easy for casual investors to trade. A bunch of people will pool their money via a broker, and that broker will buy and sell on their behalf.

Mutual and Index Funds

The two main types are Mutual Funds and Index funds, where Index funds are a subset of Mutual funds. Just like stocks, these funds will have shares that you can buy. Each of those shares will represent the basket of investments the fund contains.

Unlike normal stocks and bonds though, funds have a fee associated with holding them. This fee is called the Expense Ratio and is used to pay for any overhead associated with running the fund. The lower the overhead, the lower the fee.

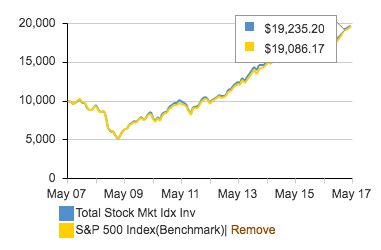

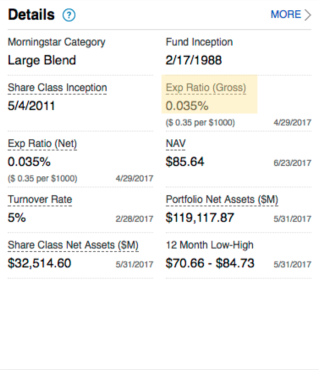

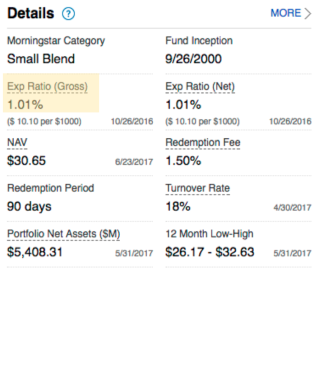

One of the easiest ways to lower fees is to not actively pick the underlying assets, and instead tie the fund to an index like we talked about above. Mutual Funds that do this are called Index Funds. On the image to the right, you can see an index fund that is attempting to track the S&P 500, and how closely it's able to do so. In this case, we're looking at the Vanguard Total Stock Market Index Fund.

Expense Ratios

As mentioned above, every fund will have an Expense Ratio. This is the Percentage Cost Per Year to participate in a given fund.

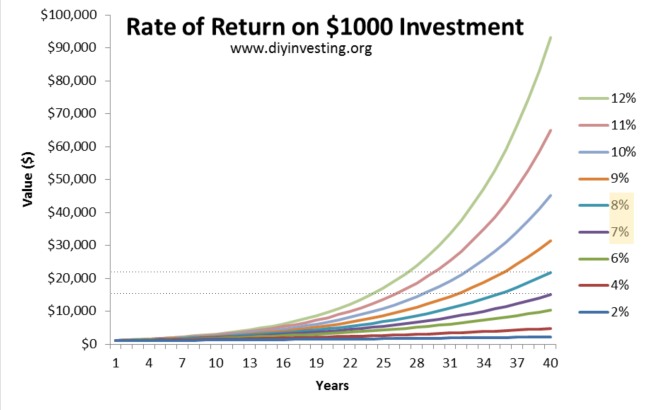

So, for example, if you buy into a fund that has an expense ratio of 1%, and the fund yields 3% this year, you'll have a profit of 2%. What does that mean in real money? Have a look below:

I've highlighted the 8% and 7% lines to show what you might find if you were in a fund that returned 8%, but had an expense ratio of 1%. In the above example, we're only dealing with $1000, but over a course of 40 years. If you follow the dotted lines back to the left axis, you'll see that there's a difference of roughly $6,000 in the returns lost to the expense ratio.

But enough theory, let's take a look at some real-life funds and their expense ratios.

So what do actual funds looks like?

The above funds are real life examples that I pulled from my company's 401k plan. In order for the fund on the right (FSCRX) to compete with the left (FXSIX), it must overcome .975% of returns.

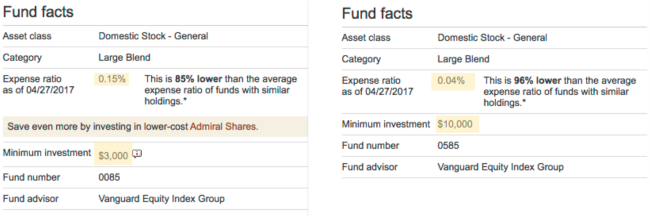

Further, some funds will give you better expense ratios when you deposit more money. In the above example I've listed two Vanguard funds that only differ in their minimum depost. On the left, a deposit between $3000 and $9999 will get you an expense ratio of 0.15%. On the right, a deposit over $10,000 will get you an expense ratio of 0.04%.

Buying a fund

There are two main ways to buy a fund: through a broker's own service, or on a stock exchange using Exchange Traded Funds (ETFs).

Through a broker's service

For this example, I'll use Vanguard, as I have experience with their process:

- Create an account

- Personal or Retirement (IRA/etc)

- Select one or more funds to throw your money at

- Many funds have several tiers, like “Investor” and “Admiral”

- “Admiral” funds require a higher minimum balance, but have lower Expense Ratios

- Set up a bank transfer for your initial deposit

- Each fund has a minimum balance, so at least that

- You can then set up recurring automatic deposits (or not)

ETFs

ETFs are funds bought and sold on a normal stock exchange. For most of the funds that a broker provides, you'll be able to find the equivalend ETF on the open market.

With ETFs, you get more flexibility in buying and selling, but you don't get the total allocation that buying partial shares gets you. If you'd like more info ETFs, I'd suggest google.

Fund Diversification

By default, when you're buying a mutual or index fund, you're getting at least some diversification of companies. Depending on the fund, you may be invested in certain Sectors like healthcare or technology, certain asset types like stocks or bonds or real estate, or certain countries and regions like the US or Asia.

You can further reduce your investment risk profile by investing in funds in these differring classes. For instance, having your money in two different US stock funds is probably less diverse than having one stock and one bond fund. Having only US assets is probably more risky than having a mix of US and International assets.

So where's a good place to draw the line? As it turns out, there's some commonly suggested approaches, at least for long-term investing. These are the (manually controlled) Three-fund Portfolio and the (automagical) Blended Funds.

Three-fund Portfolio

The idea here is to divide your investments into three investment types:

- US Stocks

- International Stocks

- Bonds

- US, International, or Both

The next question is to figure out how to balance these investment types. The most common suggestion is to do so based on your age:

- [100 - (your age)]% in Stocks

- [100 - (half your age)]% in Stocks (what I'm doing)

So, for example if you chose the second option, if you're 30, you'd have 15% of your assets in bonds, and the remaining 85% in stocks. If you are 40, you'd have 20% of your assets in bonds.

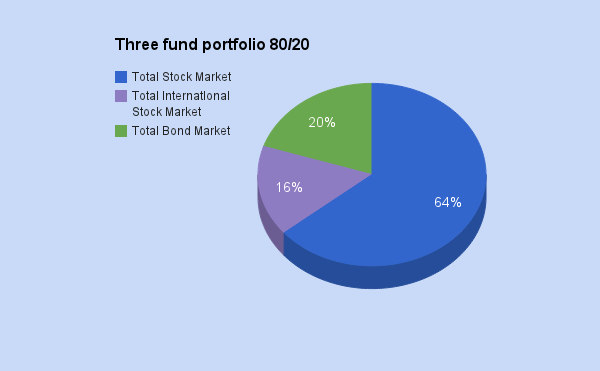

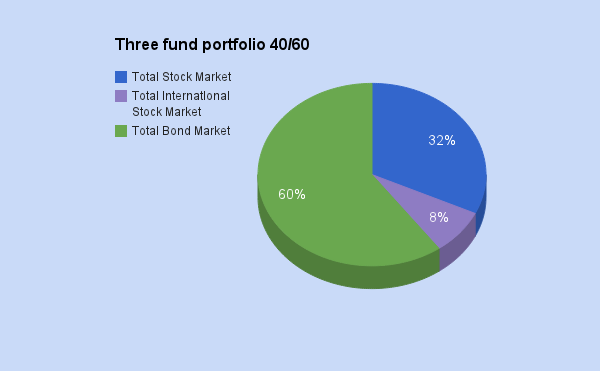

From here, you can choose the allocation of your stocks. Below, you can see I've got about 15% of my total assets in international stocks, and the remainder in US.

Blended Funds

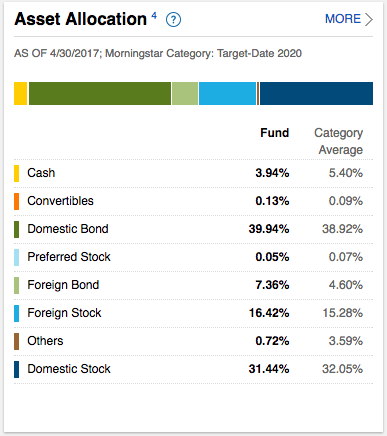

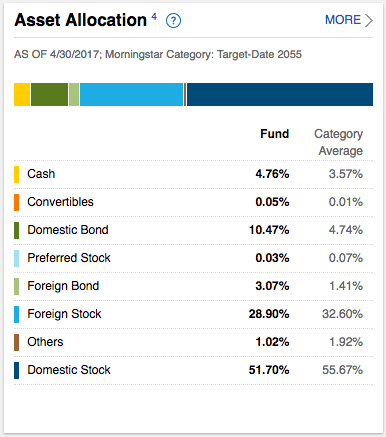

Blended funds are sometimes also called "Retirement Date" or "Target Date" funds because you will choose when you want to start withdrawing money, aka your retirement year, and then forget about it until you retire. You can usually find these on your plan by looking for the numbers in the funds names. You'll typically see a bunch of funds clustered together with names like "Fidelity Freedom 2030" or "Vanguard Target Retirement 2050 Fund".

The main draw for these funds is that, over time, they automatically rebalance from riskier stocks to safer bonds. Unfortunately, since these are automatic, they tend to cost more than doing it yourself. In the example I found in my Fidelity 401K, the Blended Funds cost more than 10-times my Three-fund Portfolio.

If you don't like the idea of paying so much for your automatic rebalancing, but also don't trust the math of the Three-fund Portfolio, then you can also try to make your portfolio look like the blended fund of your choice, since they show the current allocations. You can do this by choosing index funds at the same percentages as seen in the blended fund's information page.

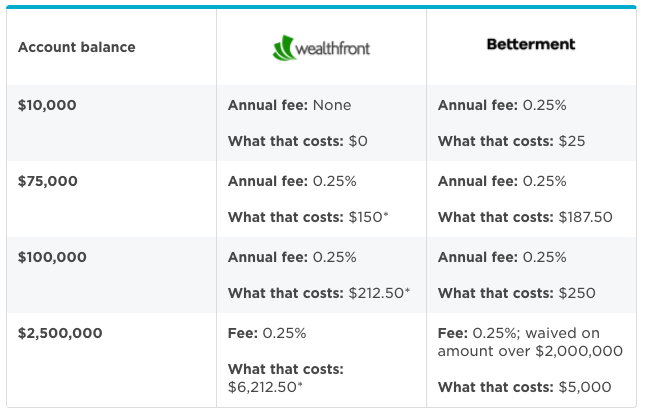

Robo Funds

There's another option when it comes to investing outside of your 401k, and that is the new(ish) concept of Robo Funds. Robo Funds are automated investments that can bring together the automated rebalancing of target date funds with a new magic called "Tax Loss Harvesting".

A look at two competing services is below:

Special Cases and Considerations

401(k)

- Pay taxes on withdraw

- Choose me if you plan on using less money when you retire

- Choose me if you think taxes will be lower when you retire

- Pay taxes now

- Choose me if you plan on using more money when you retire

- Choose me if you think taxes will be higher when you retire

I chose traditional because I think I’ll be using less money when I retire

Other people suggest having money in both because you don’t know what your tax situation will be, or all-in on roth so you don’t have to worry about taxes later on.

Company Match and Limits

If your company offers a match, you should at least contribute what you need to meet that. It's free money after all!

There's a personal contribution limit of $18,000 per year, as of 2018. If you're over 50, that limit bumps up to $24,000.

Your company can match up to 2x of your maximum contribution, bringing the total possible yearly contributions up to $54,000. Talk to your manager about that.

Employee Stock Purchase Progam

Or ESPP. Also known as...

ESPP is a program some companies offer that lets you purchase shares at a discounted rate. Here's the gist of how it works:

- Every 6 months, you have the opportunity to purchase stocks at a minimum discount of some percentage. Where I work, it's 15% so I'll use that number from here on.

- The discount is on the lesser of two prices:

- The share price on the purchase date.

- The share price on a previous purchase date.

- The minimum return is about 17.5% on this example due to maths N/(N-N*.15)

- The discount is on the lesser of two prices:

- In my program, the purchase dates are June 15th and December 15th of each year (or the closest trading day)

- You're able to contribute 2-15% of your gross income to this.

- This money comes out of each paycheck, usually up to some maximum contribution per 6-month period.

- This ends up being a very low risk, but very high reward investment

- If at all possible, you should participate in ESPP at the maximum 15%.

- Even if you have to use credit cards to finance it.

- It’s my opinion that you should sell your ESPP immediately, and put it into more diverse funds

- Being heavily invested in the company you work for isn’t ideal

- If they tank, you'd be out your investment AND possibly out of a job

- But other folks have their own opinion

An Example

You make 100K, and elect to contribute 15% towards ESPP. The June stock price was $70. Today is December 15, at 4PM, and the current stock price is $80

- You’ll set aside 15K/year ($1,250/month) of your net income, out of your paycheck.

- In june and december, you’ll make purchases for $7500 of discounted stock.

The two prices you'll be eligible to buy at are:

- 15% discount on $70 is $59.50 (June)

- 15% discount on $80 is $68.00 (Dec)

Because the June price is cheaper, you’ll buy at that rate.

- $7,500 / $59.50 = 126 shares of stock

You may then sell those 126 shares at the current price of $80

- 126 * $80 = $10,080

- With a profit of (10080 - 7500) = $2,580

- And a rate of return of 44%